Realty Executives Midwest

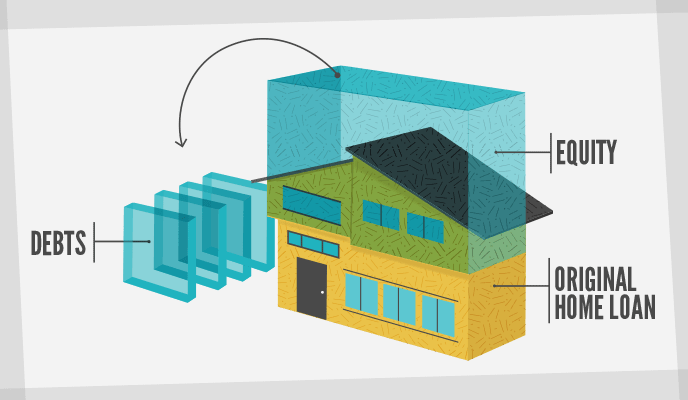

The dream of home ownership is about more than just a stable place to live, exempt from the whims and decisions of landlords. For many, home ownership is a piece of the wealth building picture, essential to a future retirement or financial independence. The idea is pretty basic: You purchase a home and pay it down while hoping the value of the home increases over time. Generally speaking, this is what happens over a long enough period of time. As you go, you build what’s called “equity.”

Equity is defined as “the market value of a homeowner's unencumbered interest in their real property—that is, the sum of the home's fair market value and the outstanding balance of all liens on the property.” If you were to sell your home and pay off the balance of the mortgage (and any other debts, such as home equity credit lines or liens), the cash you would have leftover is your equity. Your “equity position” changes over time due to a variety of factors.

As you’ve probably noted, the biggest variable in your home equity position is the home’s true market value. A variety of factors can influence your home’s value, including: Market demand for homes in your area, local amenities, schools, your home’s particular features, upgrades you’ve made, condition issues, and quite a bit more. So how can you tell your equity position?

First, you need to know what you owe on your home. This is as simple as checking your mortgage statement to see what your principle balance is on the loan. This number can differ slightly from your actual payoff amount due to closing dates, interest, and other issues determined during the sale, but generally speaking your principle balance is the number you need to know. If you have any other debt on the home, you need to add the value of this debt to the principle balance. This might include credit lines, liens, or second mortgages, for example.

Next, you need to know the value of your home. While there are sites such as Zillow and Trulia out there which will tell you what your home’s value is, these “automated valuation models” are generally not very accurate when it comes to your home’s value, as they exclude many crucial factors. Often they come in quite a bit higher. They can, however, give you an idea of general changing trends in your market over time.

Hiring an appraiser is one way to determine your home’s value from a more bank-like perspective. While an actual sale may be above the appraisal, this thorough, conservative option is a good way to go. The downside? You may have to pay up to $500 for the appraisal.

Of course, we are happy to help you get a handle on your home’s current value with a comparative market analysis (CMA). Just get in touch today.

Realty Executives Midwest

1310 Plainfield Rd. Ste 2 | Darien, IL 60561

Office: 630-969-8880

E-Mail: experts@realtyexecutives.com

Realty Executives agents are real estate experts. They have the education and expertise you need to navigate through the process of buying or selling a home. From listing at the right price to making the best offer, our Executives have witnessed the best - and most regrettable - decisions homeowners and homebuyers can make. Every day, they are immersed in every aspect of real estate that includes comparable home price analysis, property surveys, credit reports, open houses, HOA agreements, lenders, title companies, homeowners’ insurance, walk-throughs, terms of sale or purchase, repairs, concessions and closing documents. Let our accomplished Executives help navigate you through the process of buying or selling a home.